The end of the year is often a time for investors to buy and sell stocks and clean out portfolios. Some investors allocate excess cash to new investments or add to existing assets. That’s why we discuss 5 stocking stuffers for Christmas 2025.

It makes sense to review your portfolio and add undervalued stocks that potentially deliver solid total returns. Alternatively, some stocks that were overvalued for years are now more reasonably priced.

We emphasize dividend stocks and list five stocks to consider buying before Christmas 2025. Some are undervalued due to recession fears, and others face company-specific issues. But they are attractively priced dividend yields larger than the S&P 500 Index and solid dividend safety.

Partner

Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend history and much more.

Stocks to buy before Christmas 2025

S&P Global Inc. (SPGI)

S&P Global is a global provider of financial services and business information, with revenues of more than $15 billion. Through its various segments, it provides credit ratings, benchmarks and indices, analytics and other data to participants in the commodity, capital and automotive markets.

S&P Global paid dividends continuously since 1937 and has increased its payout for 52 consecutive years, and it is one of the newest members of the prestigious Dividend kings.

S&P reported third-quarter earnings on October 30, 2025. The company reported adjusted earnings per share of $4.73, which was 32 cents above estimates. Earnings rose sharply from $3.89 a year ago. Revenue rose nearly 9% year-over-year to $3.89 billion, beating expectations by $60 million.

Expenses were $2.22 billion, flat from the previous quarter and up from $2.17 billion a year ago. The adjusted operating margin increased again to 52.1% of sales.

The company entered into an agreement to buy privately held company With Intelligence for $1.8 billion. The transaction is expected to close late this year or early next year and should result in a slight dilution of earnings per share in 2026, followed by an increase in subsequent years.

We expect an annual return of 13% over the next five years.

Related articles on S&P Global on dividend power

Eversource energy (ES)

Eversource Energy is a diversified holding company with subsidiaries that provide regulated electric, gas and water distribution services in the Northeastern United States. It serves more than four million utility customers. The regulated utility is organized into the following operating segments. It’s our second stocking stuffer we’ve purchased before Christmas this year.

The Electric Distribution segment consists of the distribution operations of The Connecticut Light and Power Company, NSTAR Electric Company and the Public Service Company of New Hampshire. These subsidiaries distribute electricity to residential customers in Connecticut, Massachusetts and New Hampshire.

The Electrical Transmission segment includes transmission facilities owned by the three subsidiaries of the Electrical Distribution segment. These transmit electricity throughout New England.

The natural gas distribution segment includes the subsidiaries NSTAR Gas, EGMA and Yankee Gas. Together they distribute natural gas to more than 900,000 customers in Massachusetts and Connecticut.

Finally, the Water Distribution segment operates five separate regulated water utilities in Connecticut, Massachusetts and New Hampshire. These companies serve almost 250,000 customers in 73 towns and cities.

On November 4, ES released its third-quarter earnings report for the period ending September 30, 2025. The company’s total operating revenues grew 5.1% year over year to $3.22 billion during the quarter.

Higher basic distribution rates and continued system investments were the driving forces behind this revenue growth in the quarter. ES posted non-GAAP earnings per share of $1.19 for the quarter, up 5.3% from the same period a year ago. That exceeded analyst consensus by $0.04 during the quarter.

We expect an annual return of 13% over the next five years. ES has increased its dividend for 27 years, making it a Dividend Aristocrat. According to Stock Robber*, the future dividend yield is 4.4%.

Related articles about Eversource Energy on Dividend Power

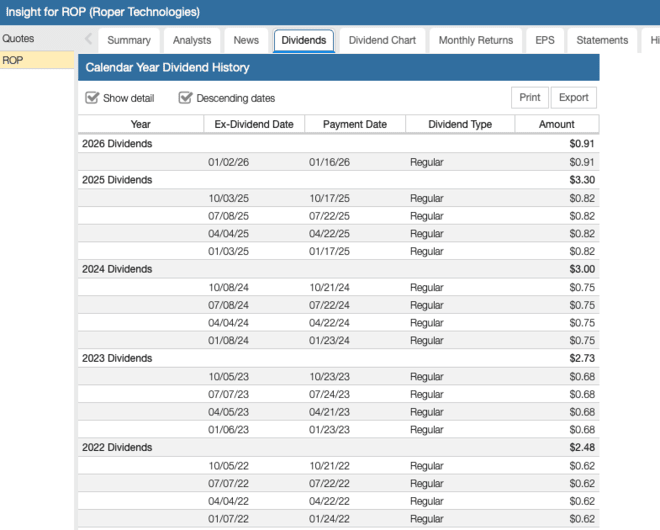

Roper Technologies (ROP)

Roper Technologies is a specialty industrial company that manufactures products such as medical and scientific imaging equipment, pumps and materials analysis equipment. It also develops software solutions for the healthcare, transportation, food, energy and water industries. The company generates annual revenue of approximately $7.0 billion.

On October 23, 2025, Roper posted its third quarter results for the period ending September 30, 2025. Quarterly revenue and adjusted earnings per share were $2.02 billion and $5.14, up 14% and 11% year over year, respectively.

Organic growth was 6%, with acquisitions contributing 8%, reflecting the continued strength of Roper’s diversified software and technology portfolio. During the quarter, the company committed $1.3 billion to strategic acquisitions, including Subsplash and several add-on deals, while continuing to advance AI-powered innovation across its operations.

Management modestly adjusted full-year 2025 adjusted EPS guidance to a range of $19.90 to $19.95 (from $19.90 to $20.05 previously) to reflect minor dilution from recent acquisitions.

We expect a 14% annual return for ROP stock going forward. ROP has increased its dividend for 32 years in a row, making it a Dividend champion.

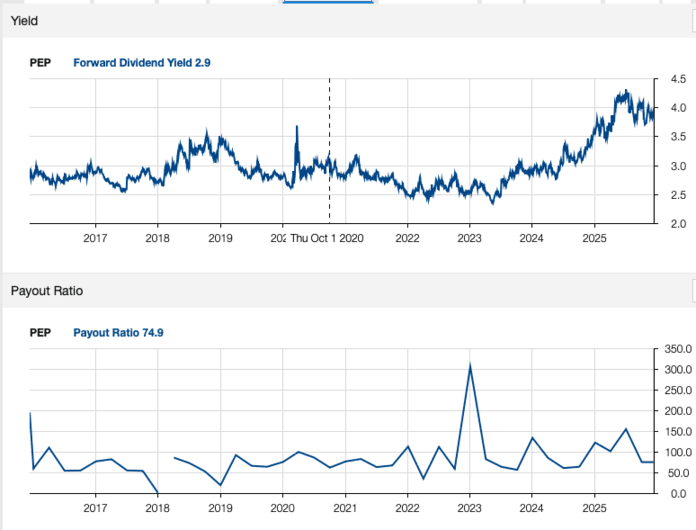

PepsiCo Inc. (PEP)

PepsiCo is a global food and beverage company with annual revenues of $89 billion. The company’s products include Pepsi, Mountain Dew, Frito-Lay chips, Gatorade, Tropicana orange juice and Quaker foods.

The company has more than 20 brands valued at $1 billion or more in its portfolio. On February 4, 2025, PepsiCo increased its dividend by 5.0% annually to $5.69, effective from the June 2025 payment, extending the company’s dividend growth to 53 consecutive years. It’s on the list of Dividend Kings.

On October 9, 2025, PepsiCo reported third-quarter earnings results. For the quarter, revenue grew 2.7% to $23.9 billion, beating estimates by $90 million. Adjusted earnings per share of $2.29 compared unfavorably to $2.31 last year, but was $0.03 better than expected.

Organic sales grew by 1.3% in the third quarter. Over the period, volumes for both beverages and food decreased by 1%. PepsiCo Beverages North America’s organic sales grew 2% during the period, while volume declined 3%.

We expect an annual return of almost 15% per year for PEP shares. The company has increased its dividend for 53 years in a row.

Related articles about Pepsico on dividend power

Brown & Brown (BRO)

Brown & Brown Inc. is a leading insurance brokerage firm providing risk management solutions to both individuals and businesses, with an emphasis on property and casualty insurance. Brown & Brown has a remarkably high level of insider ownership. It is our last stock to buy before Christmas 2025.

Brown & Brown reported third-quarter earnings on October 27, 2025, and the results were better than expected. Adjusted earnings per share came in at $1.05, which was 12 cents above estimates. Revenue rose 35% year over year thanks to acquisitions, exceeding expectations by $70 million to $1.61 billion.

Commissions and fees increased 34% year over year, while organic revenue (excluding acquisitions) increased 3.5%. Pre-tax income was $311 million, down 2% year-on-year, with margin falling from 26.7% of sales to 19.4%.

For the nine months, revenue rose 19% year-over-year to $4.3 billion, while commissions and fees rose 18%. Organic sales growth was 4.6%. Pre-tax income was $1 billion, up 2%, while margins fell from 28.4% to 24.4% of sales. EBITDAC amounted to $1.6 billion with an EBITDAC margin increasing from 35.9% to 37.1% of sales.

We slightly increased our earnings per share estimate for this year to $4.20. According to Stock Robber* the company also increased its dividend for the 32nd year in a row, by 10%, to a new payout of 66 cents per share per year.

Disclosure: No positions in stocks mentioned

Related articles about dividend power

Here are my recommendations:

Branches

- Simply Investing Report and Analysis Platform or the Course can teach you how to invest in stocks. Try it for free for 14 days.

- Free Dividend Kings Spreadsheet from Sure Dividend, complete with Buy/Hold/Sell recommendations, dividend history and much more. It’s an excellent resource for do-it-yourself dividend growth investors and retirees.

- Stock Robber is the leading investment research platform with all the fundamental metrics, screens and analysis tools you need. Try it for free for 14 days.

Get one free e-book, “Become a Better Investor: 5 Fundamental Metrics You Need to Know!” Join thousands of other readers!

*This post contains affiliate links, which means I will earn a commission for any purchases you make on the affiliate’s website through these links. This will not incur any additional costs for you. Read my disclosure for more information.

Bob Ciura

Bob Ciura is Chairman of Content at Sure Dividend. Bob has been working at Sure Dividend since October 2016. He oversees all content for Sure Dividend and its partner sites. Before joining Sure Dividend, Bob was an independent equity analyst. Bob earned a bachelor’s degree in Finance from DePaul University, and an MBA with a concentration in Investments from the University of Notre Dame.

#stocking #stuffers #buy #Christmas